Luxury in a Post-COVID World

Furniture World News Desk on

6/29/2020

I’ve spent hours digesting their reports, including interviewing Bain’s Claudia D’Aprizio, who is arguably the world’s leading authority on the luxury market, trying to get a clear picture of what to expect coming out of this global pandemic.

Loss Leaders

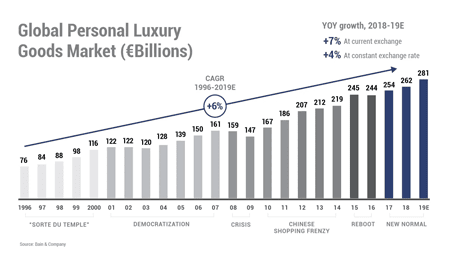

All MBBs are predicting dramatic 2020 losses for the ~$300 billion global personal luxury market, from 22 percent -28 percent by BCG to 35 percent -39 percent by McKinsey. Bain is hedging its bets with the broadest range between 20 percent to 35 percent lost in 2020.

But Bain goes further, predicting the industry will recover to 2019 levels by end of 2022 or early 2023, then power ahead over the next two years to reach $347 -$358 billion on 14 percent to 17 percent growth.

D’Aprizio admits predicting the future for luxury coming out of this crisis is particularly problematic since it impacted not just consumers’ financial wellbeing, but their health and emotions. “It’s probably going to have more than double the impact that the industry had from 2007 to 2009,” she says.

And that’s the essential problem with all the financial models the MBBs are dishing out, whether they are U-shaped, V-shaped, or the new darling proposed by Bloomberg, Nike-swoosh shaped. Economists look at numbers and history to build their predictive models. The variable missing is the psychological impact of the coronavirus pandemic on consumers and you can’t graph that because feelings can’t be translated literally into numbers or dollars.

Predicting the future for luxury coming out of this crisis is particularly problematic since it impacted not just consumers’ financial wellbeing, but their health and emotions.

“Consumption is driven by very strong motivations, like emotion, identity, and social connection. Those motivations aren’t going anywhere,” explains Erica Carranza, PhD and vice president of consumer psychology at research firm Chadwick Martin Bailey. “But the values, habits, and norms that shape what we consume and how we consume could shift dramatically.”

World Events Shape Generational Values

William Strauss and Neil Howe have been widely praised, and equally widely lambasted, for their Generational Theory that postulates world events occurring at formative stages of each generation’s development shapes their views of the world and sets the course for the trajectory of their lives.

The Baby Boomers were energized by Beatlemania and Woodstock, and then their optimism was rocked by the Kennedy assassination, civil rights, and the Vietnam War — followed by Watergate, the oil crisis and economic stagnation of the 1970s.

Often called the overlooked generation, GenXers’ defining experiences included the stock market crash and recession in the 1980s, followed by the dot.com bubble in 1999, 9/11 and the Great Recession in 2008.

The millennials, born 1982 to 2004, were emotionally seared by September 11, 2001 – similar to the Boomers on November 22, 1963. Both these world events are forever burned in the memories of these two groups. And for GenZ as well as the older millennials, the long, slow recovery from the Great Recession set the economic and psychological tone of their future.

A Global Outlier

Now a truly unprecedented global crisis, the coronavirus pandemic, has xxx all generations, all over the world, all at the same time. That alone is astonishing. No generation is immune, no demographic is safe, and no worldview is exempt. Given their younger ages when values and attitudes are still forming, the millennials, GenZ and Viral generations will be more psychologically affected by the Covid-19 crisis than their older counterparts.

And this simple fact will greatly influence the prospects of the luxury market, not just for the near term, but the decade to come. We’ve already seen millennials’ and Gen Z’s disruptive influence on the luxury market over the past several years.

With a massive generational disparity in affluence from Boomers and GenXers to millennials and GenZers — many of whom have lost their jobs, or their employers have been shut down — the lasting psychological effects of coronavirus are going to set the tone for their spending for years to come.

“These are both the luxury consumers of today and tomorrow. They are a wave shaping and creating luxury brands’ evolution in terms of messaging and purpose,” D’Aprizio says. “I see these consumers a very positive underlying driver for luxury success, as long as brands stay in tune with the next generations.”

Staying in tune with the next generations will require a deep understanding of their consumer psychology.

The Ends Determine the Means

“Shopping behavior is always a means to an emotional-based end,” explains Chris Gray, PsyD., founder of consumer psychology consultancy Buycology and one of the early pioneers in the shopper psychology field with Saachi & Saachi.

“Behaviors happen for a reason, always,” he continues. “If you can get to the bottom of why – the reason it is happening – you can start to understand consumer behavior.”

Since emotions are at the core of luxury consumer spending, the luxury industry is largely dependent upon their customers’ feelings to make sales. Rational decision-making takes a back seat in the world of luxury. “We are feeling a sense of insecurity at a very basic level. The intensity of that anxiety is new to most of us,” he says, and adds customers can only manage that level of anxiety for so long.

“People get worn out. They react with a desire to buy things that show the world that they are here and safe. After an emotional crisis, the rebound is about identity building and showing the world that you are in a good place,” Gray explains. This will then lead to more identity-building and personal-reinforcement purchases, of which luxury brands are the pinnacle.

“Showing your identity is a very important emotional aspiration that plays into shopping behavior. Luxury says to the world that I’m doing well and that I can afford this. From that comes a greater sense of comfort and security,” he believes, and continues, “The spending that comes after hard times is more about identity and security.”

That’s the reason we are seeing headlines now about how Chinese consumers have emerged from quarantine ready to spend and spend lavishly.

Anxiety Will Persist

But that short-term backlash spending, or as some call it reward spending, is not going to last, suggests Michael Baer, Ipsos senior vice president and managing director U.S. Ipsos Affluent Intelligence, based upon how affluent consumers behaved after the 2008 recession.

Ipsos found that affluent’s feelings of financial anxiety persisted long after the recession recovery. From 75 percent of the affluent who were “very worried” about the state of the economy in 2009, there was only a 10-percentage point decline by 2011, when 65 percent remained in a very worried state.

Since the global financial ramifications of coronavirus have yet to be realized, it is predicted to be worse all over the world – even China — than that experienced in the 2008-2009 financial meltdown. That’s why Baer advises, “[The] anxiety and a healthy paranoia are likely to linger – possibly for a long time.”

Further, affluent’s extended financial worries played out in pronounced changes in their discretionary purchase behavior. Affluent consumers’ attitudes toward fashion purchases didn’t change overnight and took a gradual downturn and remained depressed … even while the recovery was well underway.

“This suggests that early on in the crisis, consumers were still clinging to their attitudes – but the economic context then caused them to change behaviors,” he writes. “And those behaviors stayed changed even as the economy came back.”

Baer concludes, “The key takeaway is to recognize that consumers are going through anxiety – which will in turn lead to behavioral shifts – and this won’t likely snap back to pre-crisis norms, post-crisis.”

What Comes Next

As I look across the luxury consumer market, luxury brands can count on their rich customers to come back ready to spend. But that will not be the case for the younger mass-affluent consumers, called the HENRYs (high-earners-not-rich-yet).

HENRYs occupy the space between the middle-income consumers ($50,000-$99,000) and the ultra-affluent elites ($250,000+) in the U.S. And young HENRYs are found in every country across the globe.

While individually HENRYs don’t have the spending power of the ultra-affluent, the way outnumber them as a group.

There are 32.7 million U.S. HENRY households compared with 6.2 million ultra-affluent. Over 80 percent of the nation’s nearly 40 million affluent households are HENRYs, which is why luxury brands depend upon HENRYs to keep their sales strong and growing.

In the new-normal, post-coronavirus world, the luxury market is going to be profoundly changed by pervasive changes to the young HENRYs mindset, priorities, and values. What I foresee is a dramatic shift toward wellbeing, across the dimensions of physical, emotional, and financial health and security.

First In, Last Out

Throughout the world, luxury was the first sector to experience a cutback when coronavirus hit. And after it’s over, it’s likely to be the last out of the woods.

And that’s because the young HENRYs as they emerge from their cocoons, where they have had ample time to reflect on what’s most important to them now and in the future, their spending habits are likely to make a radical shift.

Rather than indulging in luxury goods as much as their income allowed as before coronavirus, they are going to turn to saving with only an occasional indulgence in more modest, discreet luxuries where high-quality and long-lasting utility take precedence.

Securing a financially healthy future is going to be a priority for next-generation luxury consumers, with the experience from the painfully slow 2008/2009 recession still fresh in their memories. While the ultra-affluent elites may feel their financial status is immune from the aftermath of the coronavirus, the professional class HENRYs certainly don’t.

With 30 million Americans now unemployed, the AP reports that layoffs and pay cuts are starting to impact white-collar professionals at law and, accounting and consulting firms, in healthcare, marketing and administration, even professionals working in technology, design and scientific fields, like architecture and engineering.

And then there are the 16 million self-employed Americans and the 31 million small-business owners who have seen their revenues and incomes cut dramatically. These people overwhelmingly make up the HENRY demographic.

Forward March

For luxury brands, their future growth is going to come down to the 80/20 rule. About 80 percent of their target customers are HENRYs and while HENRYs may not contribute 80 percent of their revenues, it’s reasonable to assume that the HENRY’s share is way too important to lose.

But lose them they will, if the last recession is any indicator of the impact of coronavirus on the personal luxury goods market, which declined from $190 billion in 2007 to $168 billion in 2009, according to Bain.

That 10 percent decline may be a drop in the bucket compared to the aftermath of the coronavirus pandemic, which threatens not just luxury consumers’ financial status, but their personal health and emotional wellbeing as well.

About Pam Danziger: Pamela N. Danziger is an internationally recognized expert specializing in consumer insights for marketers targeting the affluent consumer segment. She is president of Unity Marketing, a boutique marketing consulting firm she founded in 1992 where she leads with research to provide brands with actionable insights into the minds of their most profitable customers.

She is also a founding partner in Retail Rescue, a firm that provides retailers with advice, mentoring and support in Marketing, Management, Merchandising, Operations, Service and Selling.

A prolific writers, she is the author of eight books including Shops that POP! 7 Steps to Extraordinary Retail Success, written about and for independent retailers. She is a contributor to The Robin Report and Forbes.com. Pam is frequently called on to share new insights with audiences and business leaders all over the world. Contact her at pam@unitymarketingonline.com.